How to Save Money to Buy a Home

Save Money to Buy a Home is the single biggest investment for most families. For many of them, it takes years to save enough money for the down payment. Factors such as an ever-changing housing sector, skyrocketing market prices, and high inflation add to problems when purchasing a house. Inflation, above all, has been the most prominent factor that has caused a sudden rise in property prices.

Feeta.pk, Pakistan’s smartest property portal, has compiled a guide that can help you save money to buy a home.

Tips to Save Money:

The following are some of the most effective tips that can help save money to buy a home as well as make the following payments:

- Break down the payments

- Eliminate your debt

- Create a budget

- Set saving goals

- Spend to save

- Choose a cheaper place

- Find new ways to generate income

- Find new ways to generate income

Break Down the Payments:

Whether you are a first-time property buyer or a regular investor, you will have to break down payments that you are required to make at various steps. Therefore, you must consider each factor while making the calculations.

The most important and difficult payment while purchasing a property is the down payment. In most cases, it is usually around 2-30% of the total cost of the property.

If you are depending on a mortgage or loan payment, it might be even trickier. Most lenders will give you money if you possess a minimum of 10% of the price of the house. Even once they lend you money, you would have to repay the amount at a specific interest rate later on.

There are also closing costs that need to be paid while completing the sales process. These can put a burden on your budget during and after the purchase. The following factors can add to the closing cost:

- Inspection costs

- Appraisal costs

- Title services

- Property insurance

- HOA (Homeowners Association) Fees

- Moving charges

- Renovation and maintenance

- Government and local body taxes

Eliminate Your Debt:

Most home buyers have to save money for years to buy their first home. Moreover, they have to manage money for various daily expenses as well. It leads them to take loans from banks or other money lenders, disrupting their savings amount.

So, if you are trying to save money through budgeting and still have a large debt burden, you need to pay it off first. Most money lenders take interest while you repay them the amount. Once you eliminate all the debt, you can add that money to your savings account.

Secondly, prioritizing your debt payments earlier will help you in managing other financial obligations later on.

Create a Budget:

The most important strategy to save money for any purpose is to have a budget plan. Whether you have a single source of income or multiple sources, if you don’t plan your budget, you will end up wasting all your money. A budget will help you to:

- Manage your expenses effectively

- Allocate appropriate resources to wants and needs

- Monitor your objectives

- Make confident financial decisions

- Identify problems of over-budgeting

However, creating a budget is not a simple task. For that, you need to consider all your expenses, future goals, and income, along with many other factors. The following checklist can help you create a realistic budget:

- Gather your financial paperwork

- Calculate your income

- Create a list of monthly expenses

- Set realistic goals

- Calculate your monthly income and expenses

- Make adjustments to the budget

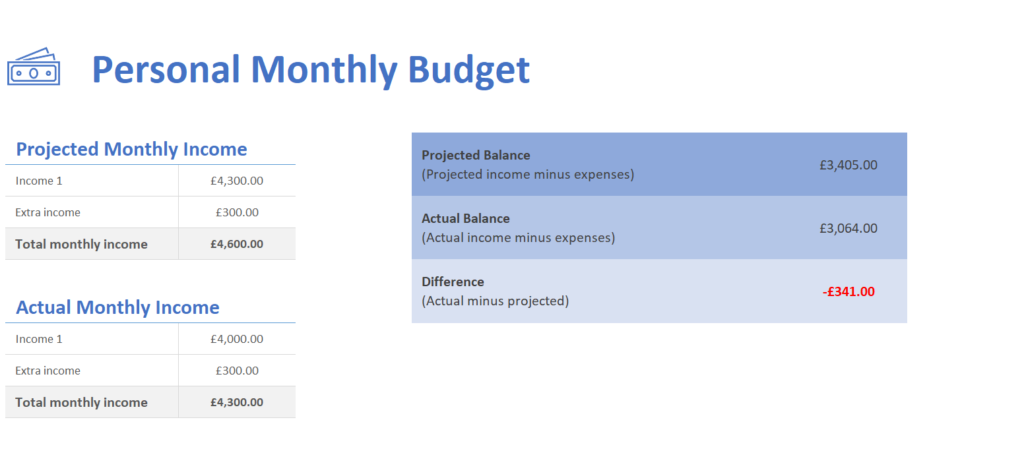

Step 1: First, calculate your income from all sources. In this manner, you will be able to divide your income equally for various expenses.

Source: MS Excel

Step 2: Secondly, list down all your expenses and keep track on a daily basis.

Source: MS Excel

Step 3: Sum up the overall budget at the end of the month.

Source: MS Excel

The difference between the budget set and the total money spent will help you in reviewing your plan. You would be able to check if your expenses will be over the budget and how you can save more money.

Set Saving Goals:

Without setting proper financial goals, budgets are likely to fail. Your financial goals can be of two types: short-term or long-term goals. Achieving short-term financial goals by managing your income and expenses will help you in achieving your long-term financial goals.

You can use the 50/30/20 rule to set realistic saving goals. Define 50% of your total monthly income for your daily needs, 30% for your wants, and save 20%. This rule will help you in the first step by allocating the budget for specific purposes.

Now, you need to check the area where you are wasting your money. If you are spending too much on your needs or wants, you should cut a specific percentage from them and add it to your savings.

Luxury items and food from restaurants account for the most percentage of your budget. You can also cut these expenses by reducing your purchase of luxury items and cooking food at home. This will increase your savings over time.

The following measures can help you achieve all your saving goals:

- Go shopping with a smarter list and shop.

- Avoid unnecessary trips to the markets.

- Prefer to eat at home.

- Eliminate unnecessary bills.

- Use less electricity and gas.

- Pay your bills on time to avoid penalties.

- Use public transportation.

- Cut the cost of your water bills.

- Trim down your daily expenses.

Spend to Save:

Source: Readers Fusion

When you buy a home, there can be several problems. For instance, there can be issues with water pipelines, electric wiring, paint, doors, windows, etc. If you ignore these repairs at first, they will eventually cost you more in the future.

You can also hire certified professionals who can give you an overall efficiency report of everything inside and outside the building. You can follow the given checklist to assess the condition of the property:

- Water damages

- Damaged roof

- Faulty electrical system

- Plumbing problems

- Structural and foundational issues

- Pest infestation

- HVAC system problems

Choose a Cheaper Place:

Property prices vary from area to area. Property prices are usually higher in densely-populated areas with a large number of commercial set-ups. On the other hand, in new residential areas with less population and small commercial set-ups, property prices are very low. Thus, you need to make a conscious decision while choosing the location.

The following are some benefits of buying a cheaper property:

- There is less competition for cheap properties as they are located in less prosperous areas.

- Cheap properties are suitable for cash investors.

- They minimize stamp duty bills.

- Cheap properties require low deposits, low payments, and low interest.

- There is a lower risk of loss of investment if you have to sell the property.

- These properties have good rental prospects.

- You will have control over all the updates and improvements.

Find New Ways to Generate Income:

Depending solely on one source of income might not help you these days in saving money. With the high inflation rate, the prices of everyday commodities have gone up. Moreover, this inflation has changed the real estate market with soaring prices. So, one must find ways to earn and save money for future investment goals.

The good news is that the internet has already provided hundreds of ways to learn and earn money online. The following are some of the ways that can help you generate income apart from a single job:

- Become a freelancer

- Become a virtual assistant

- Start an eCommerce business

- Write online reviews

- Start your own blog

- Sell photography

- Become a rideshare driver (Uber, Careem)

- Rent out items

- Manage other people’s properties

- Invest in stocks

- Become a digital creator

- Start a coaching business

There are also several other resources that you can invest in to save money to buy a home.

For more information about saving money, visit Feeta Blog.

How to Save Money to Buy a Home

Year 2022-23 Budget taxes and impact on Real Estate sector of Pakistan

Finally, Pakistan’s highly anticipated Budget taxes for the years 2022-23 is here, and as expected, there have been some major policy changes in the financial bill for 2022-23, especially in relation to the real estate sector. If you are confused about how new taxation in the budget will affect the real estate sector, I will try to explain most of them in this blog.

To understand the real impact of taxes in Budget 2022-23 on real estate, we will have to divide the real estate sector into 3 segments. The Government did the same. This was especially done to promote some segments of real estate and discourage investment in others. While some policies affect all three segments, others don’t and that’s why we need this segmentation, as it will help us understand where to invest in the coming year.

- Sector of plots and files, where there is no construction on the land.

- Construction sector like houses etc.

- Tall apartments etc.

The Government of Pakistan, in budget 2022-23 has announced three major policies regarding taxation of these segments. Don’t worry if you can’t understand them now, because I’ll explain them one by one:

- The withholding tax was revised for all three segments.

- Capital gains tax and its implication have been revised for all of the above segments.

- Real estate will be taxed on a considered rental income basis above 25 M.

Increase in withholding tax

Withholding tax is paid by the buyer of the property before they deliver the plot on their behalf. This is the only common factor that will affect all three properties similarly. In the Budget 2022-23 Government increased the withholding tax to 2% for archivists and 5% for non-declarants from 1% and 2% for archivists and non-declarants previously.

This is a significant increase, especially for non-filers. This will significantly increase the cost of transferring plots as follows:

Suppose that any property, whether it is land, house or apartment in Pakistan, has an FBR value of 1 crore, then the change in the withholding tax will be as below:

According to previous rates:

File would pay: 1 Lacquer as tax

Non-declarant would pay: 2 Lacquers in tax.

According to revised rates after July 1, 22:

Filer would pay: 2 Lacs tax

A non-declarant would pay: 5 Lacs tax.

Impact on real estate:

Generally, an increase in withholding tax means an increase in transfer costs and the real estate market views an increase in transfer costs as a negative factor for real estate.

However, in this case, I don’t see this as a major reason to impact or trigger a real estate trend. This is a one-time cost and although it will discourage short-term trading, it will be acceptable for most investors.

Capital Tax and its implications:

This is where tax policies are different for all three segments of real estate that we described at the beginning of this blog. Let’s first understand what CGT is, CGT means capital gains tax, this tax is applicable only if you have made a profit from your real estate investment.

- Plots/files: CGT will apply if you sell land 6 years ago, and are exempt after 6th year.

- 15% CGT where the holding period does not exceed 1 year.

- 12.5% CGT where the holding period exceeds 1 year but does not exceed 2 years.

- 10% CGT where the holding period exceeds 2 years but does not exceed 3 years.

- 7.5% CGT where the holding period exceeds 3 years but does not exceed 4 years.

- 5% CGT where the holding period exceeds 4 years but does not exceed 5 years.

- 2.5% CGT where the holding period exceeds 5 years but does not exceed 6 years.

- 0% CGT where the holding period exceeds 6 years.

- House / built property: CGT will apply if you sell a house 4 years ago, and are exempt after 4th year.

- 15% CGT where the holding period does not exceed 1 year.

- 10% CGT where the holding period exceeds 1 year but does not exceed 2 years.

- 7.5% CGT where the holding period exceeds 2 years but does not exceed 3 years.

- 5% CGT where the holding period exceeds 3 years but does not exceed 4 years.

- 0% CGT where the holding period exceeds 4 years.

- Apartment/hill: 15% CGT will apply for the first year and 0% tax from the 2nd year.

- 15% CGT where the holding period does not exceed 1 year.

- 7.5% CGT where the holding period exceeds 1 year but does not exceed 2 years.

- 0% CGT where the holding period exceeds 2 years.

Impact on real estate of Pakistan

As you can see clearly the focus of CGT is unproductive assets like plots and files, while the impact on the construction or building sector such as houses etc has hardly been reviewed, in addition, the apartment sector has been encouraged.

La FBR team openly stated that the reason for adopting this policy for CGT is to encourage people to invest in flats and vertical growth and therefore we can safely assume that future policies of the Government will also be in a similar direction.

Considered rental income on the unproductive property:

Now, this is a new name for wealth tax and the only real purpose for this tax is unproductive properties, such as plots and files. FBR imposed 1% Deim Tax according to the FBR value on the unused/additional property worth more than 25 M. This includes unused houses, plots of land, farmhouses, or any landed property that has a value above 25 M but does not create a regular income. The Government has estimated the income from the such property at 5% per annum, of which 20% will be taxed, which turns out to be 1% of its FBR value.

The house in which you live is exempt from this tax except that 25 M value of the property is also exempt from it. Some of the important things to keep in mind about this supposed rental tax are as follows:

- Your personal house is exempt from this tax.

- It will be levied on the collective FBR value of all your plots, for example, if you own 10 plots that have a collective FBR value of 100 M, the first 25 M will be exempt from tax and the remaining 75 M will be taxed at 1% of FBR value which amounts to 7.5 lacquers per year.

- If you have a built property, house, business, etc. that is not rented, you will have to pay the estimated rental income tax on it.

The main purpose of this tax is for the richest among us who invest in dozens of plots of land that do not produce rental income and houses that they have rented etc but do not declare their rental income.

In addition, this tax also applies if a property is rented as follows:

- If the tax under section 15 of the income tax prescription is more than the tax under this section, then no further tax will be charged.

- If the tax under section 15 of the income tax return is less than the tax under this section, then the difference in amounts shall be paid under this section.

Impact on Pakistani real estate:

The plot sector will get the most success because they do not produce any rental income and therefore will become liable. The people who have accumulated such wealth can certainly pay this amount of tax, but future investment in non-rent producing real estate will certainly be a great success.

While the smaller societies for the lower middle and middle class, can show some resilience and turn out untouched. Wealthier societies, such as DHA, and Bahria Town, where investors have invested huge amounts, will tremble. And after the big boys fall, the impact will be felt in the smaller societies as well.

The focus is to discourage investors from holding more than 25M of unproductive assets such as plots, files, houses, farmhouses and so on.

Analysis:

The current Pakistan budget for 2022-23 and its impact on real estate will be as follows:

- It is very negative for land, files, farmhouses or any other unproductive property, so I will assume that if these policies remain unchanged, we will enter a downturn in this segment.

- For buildings built on the waterfront such as houses or commercials, it is a good budget because most things are unchanged and the continuation of policy is always good.

- The apartment sector was highly motivated with exemption from CGT after the second year and in addition if rented as built-in property, considered rent income tax also does not apply as long as you pay tax according to section 15 of income tax. This is the sector that will attract the most investment under these new policies.

That is why I believe the Government wants investors to shift real estate trading and investment to apartments and high-rise buildings or to real businesses and industry.

You should also remember that the DC values are expected to be reviewed by the provincial government as well.

I warn against such a move by Govt to target unproductive assets like plots and files etc since the second half of 2021. The real target is wealthy people as investors who only hold 25 M values per FBR value in addition to their value. homes are exempt from certain taxes.

The current budget is clearly in line with the IMF and FATF plans to discourage investment in plots and files that are considered unproductive assets.

You now have three options if you want to make money in real estate.

- Move your investments to apartments/elevators.

- Invest in rental farms.

- Expect a miracle for the Government to withdraw from these policies.

Also, if you want to read more informative content about construction and real estate, keep following Feeta Blog, the best property blog in Pakistan.